In fact, Australia is on the brink of a property boom if recent forecasts are anything to go by. Commonwealth Bank believes house prices will rise by 16% in the next two years, while Westpac went a step further, predicting a 20% surge.

It’s a far cry from the start of the COVID-19 pandemic when every man and his dog were predicting Armageddon with enormous house price drops of up to 40%.

-

Related: How accurate were Australians' COVID house price predictions?

-

Related: Here’s why Australian property prices didn’t crash in 2020

-

Related: What will happen to Australian house prices in a recession?

Of course we now know that house prices actually remained pretty stable during COVID, only falling by -2.1% nationally between April and September 2020 before rebounding.

The most recent home value index results from CoreLogic shows national house prices surged 2.1% in February, marking the biggest month-on-month change in 17 years.

Buying a home or looking to refinance? The table below features home loans with some of the lowest interest rates on the market for owner-occupiers.

| Lender | Home Loan | Interest Rate | Comparison Rate* | Monthly Repayment | Repayment type | Rate Type | Offset | Redraw | Ongoing Fees | Upfront Fees | LVR | Lump Sum Repayment | Additional Repayments | Split Loan Option | Tags | Features | Link | Compare |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

6.04% p.a. | 6.06% p.a. | $2,408 | Principal & Interest | Variable | $0 | $530 | 90% | Featured 4.6 Star Customer Ratings |

| |||||||||

5.99% p.a. | 5.90% p.a. | $2,396 | Principal & Interest | Variable | $0 | $0 | 80% | Featured Apply In Minutes |

| |||||||||

6.09% p.a. | 6.11% p.a. | $2,421 | Principal & Interest | Variable | $0 | $250 | 60% | Featured Unlimited Redraws |

|

‘Perfect storm’ driving up house prices

Analysts say this is due to a ‘perfect storm’ of historic low mortgage interest rates, a stronger than expected economic recovery, and strong buyer demand against relatively low levels of stock.

The number of properties advertised for sale nationally remained 26.2% below 2020 levels over the 28 days ending February 21.

CoreLogic research director Tim Lawless said the mismatch between supply and demand is one factor pushing up house prices.

“Housing inventory is around record lows for this time of year and buyer demand is well above average. These conditions favour sellers,” Mr Lawless said.

“Buyers are likely confronting a sense of FOMO (fear of missing out) which limits their ability to negotiate.”

This fear of missing out has become a powerful driver for first home buyers as record low interest rates and government incentives including the First Home Loan Deposit Scheme (FHLDS) and HomeBuilder are encouraging buyers to race into the market.

But the Real Estate Institute of Australia (REIA) has warned the combination of increased buyer demand and rising house prices could “obliterate” housing affordability.

“Australian first home buyers increased their market share by 50.4% over 2020, motivated by low interest rates and the range of first home buyer incentives on offer,” REIA President Adrian Kelly said.

“Seeing this trend in conversion to home ownership is particularly great news given the challenges many tenants and investors faced over the pandemic however surging house prices could see housing affordability obliterated unless measures to improve supply are implemented.”

According to the latest ABS lending statistics, first home buyers now make up almost half (41.6%) of owner occupier dwelling commitments, after a 70.8% rise in the number of loans to first home buyers between January 2020 and January 2021.

Soaring house prices puts home ownership further out of reach for first home buyers

One of those first home buyers is Brisbane man Matthew Farnham, who has been looking for his first home with his partner since mid-January.

“It’s only been in the last couple of weeks the property market seems to have really exploded. Properties that would have been under $500k are now going for mid $500’s.”

The couple are firm on their $500k budget because they’re using the first home stamp duty concession, which waives stamp duty costs on properties up to $500,000.

“It hinders us because we have to stick with a purchase price of $500,000,” he said.

He says their savings slowed down a bit during COVID when his partner, who works at Flight Center, had his hours reduced.

“He’s still on four days a week and waiting to hear when he’ll go back to full time,” Matt said.

“The bank we went with was happy to accept the reduced income because he had been reduced to four days a week in June or July and it had just stayed at that, whereas other banks were like ‘no he’s on reduced hours so we’re not accepting that'.”

While he’s optimistic they’ll eventually be able to get into the market, Matt says they should have bought last year when there was speculation house prices would go down.

“I wish we had been seriously looking at the end of last year because we looked at a couple of properties at the end of last year and ummed and ahhed. We said we would just renew our lease for another six months and keep saving and look in the New Year.

“In hindsight, we should have bought last year.”

*Since writing this article, Matt and his partner have signed a contract on a three-bedroom townhouse in an outer eastern suburb of Brisbane, which was slightly further out than where they had originally been looking, but within their original $500k budget*

Someone who did buy last year is 26-year-old Natalie and her partner Jake.

The couple bought land in the Sunshine Coast’s Mooloolah Valley in August last year, and finished construction in January.

“We had engaged a broker, and then we started to hear in the media the announcements of the First Home Owner Grant and the Home Builder grant, so we spoke to our broker about these schemes,” Natalie told Savings.com.au

“Our broker took the lead on this to make sure that we would be eligible and make sure we had the best chance of getting access to the schemes and grants.

“We ended up using both the First Home Owner Grant and the HomeBuilder Grant.”

The couple, who had been saving for three years, decided to pull the trigger on their decision to buy a home after COVID forced them to postpone their wedding plans.

“We decided to buy a home first and get married later on so we spent our wedding money on the property and built our home,” Natalie said.

“We wanted to speak to a broker because of the commotion around the news of the property market – depends on where you are but I understand prices on the Sunshine Coast are pretty crazy at the moment.”

Property prices are rising so fast at the moment that buyer’s agent Wendy Chamberlain says buyers are having to significantly increase their budgets just to keep up with the market.

“I’m working with a first home buyer client that is being priced out of the areas she wishes to buy,” Ms Chamberlain told Savings.com.au.

“Even just this weekend, two homes that she could have afforded earlier in 2021 sold for $35,000 and $51,000 above the vendor's reserve price.”

She says another client who is looking to buy into a particular school area will have to up their budget by at least $300,000 if they want to buy close to the school.

Buyers having to make “sobering decisions”

With no sign of the market cooling off anytime soon, Ms Chamberlain says buyers need to be prepared to significantly adjust their expectations.

“Those that cannot [increase their budgets] need to look for homes that they can afford. Expectations on location and the type of home or state of repair now need to be considered,” Ms Chamberlain said.

“A buyer may have to consider buying a home that requires a renovation versus something that has already been renovated. Buyers may also have to consider looking in a suburb or two over from where they ideally would love to live.

“Buyers are having to make sobering decisions about where to buy and also the type of home to buy. A three-bedroom home on land may now only look like a two-bedroom villa unit due to budget constraints.”

She says first time buyers need to remember they’re not buying their forever home.

“In a rising market like the one we are seeing, sometimes there is merit in getting in the door and on the property ladder now, with the possibility of enjoying some capital growth in the shorter term.

“Then, down the track, a home that is better suited to your longer term needs and goals can be considered.

“Those that can, are tapping into the bank of mum and dad, but not every first home buyer has that option.”

Aussie home loans chief customer officer David Smith says those trying to get into the market need to gain the competitive edge.

“It’s important to know where to look, get your pre-approval, and financing plan sorted; so you can have the upper hand against other potential buyers,” he told Savings.com.au.

However, not all buyers are securing finance before making an offer.

Upside Realty National Sales Director James Kirkland told Savings.com.au properties are going under contract and then quickly being put back on the market because some buyers are rushing to make offers before they’ve been approved for a loan.

“With such low stock currently available, many buyers are feeling the pressure to perform and, in many instances exceeding their budget, before they have their official finance approval,” he said.

“While we are certainly aware that this is happening at the moment - due to a surge in buyer activity and a real ‘fear of missing out’ - we would strongly discourage our vendors from accepting any offers that are not qualified or pre-approved; hence why auction is such a good method of selling property.”

Buyers could also consider enlisting a buyer’s advocate who have access to homes off market, or tapping into resources like Domain’s off-market properties to get an early look at potential properties in their area before they hit the market.

Will runaway house prices force RBA or APRA’s hand?

The Reserve Bank Governor Philip Lowe has reiterated it is not the responsibility of the RBA to target housing prices.

"I recognise that low interest rates are one of the factors contributing to higher housing prices and that high and rising housing prices raise concerns for many people," Dr Lowe recently told an Australian Financial Review business summit.

"There are various tools, other than higher interest rates, to address these concerns, leaving monetary policy to maintain its strong focus on the recovery in the economy, jobs and wages."

CoreLogic’s head of research, Eliza Owen agreed that despite the RBA’s policies influencing house prices, it wasn’t their job to intervene.

“To an extent, rising house prices are a way low interest rates work to stimulate the economy, because it creates a wealth effect among home owners," she told Savings.com.au earlier this month.

"Institutions that would have the responsibility of monitoring market conditions would be the Australian Prudential Regulation Authority (APRA), who keep an eye on prudential standards in lending, and government, who would have an interest in addressing barriers to home ownership."

Dr Lowe said the RBA will continue to pay attention to lending standards.

"Looser standards would increase medium-term risks and add to the upward pressure on prices, so would be of concern," he said.

"Reflecting this, the Council of Financial Regulators (CFR) has indicated that it would consider possible responses should lending standards deteriorate and financial risks increase. We are not at this point, but we are watching carefully."

The CFR is the coordinating body for Australia’s main financial regulatory agencies: Treasury, the RBA, the Australian Securities and Investments Commission (ASIC), and APRA.

APRA could be forced to reintroduce macro-prudential measures, such as loan-to-value-ratio (LVR) caps, to slow the rate of lending as they did in 2017 if house prices continue surging.

Across the ditch in New Zealand, property prices surged 2.6% in February according to CoreLogic data, building on January’s gains of 2.2% which culminated in New Zealand’s reserve bank implementing restrictions on mortgage lending.

From the start of this month, banks can only allocate 20% of new lending to loans with an LVR over 80%, and a maximum of 5% of new lending at LVRs above 70% for investors.

From May, LVR restrictions for investors will be further raised to a maximum of 5% of new lending at LVRs above 60% (so investors have to stump up a 40% deposit).

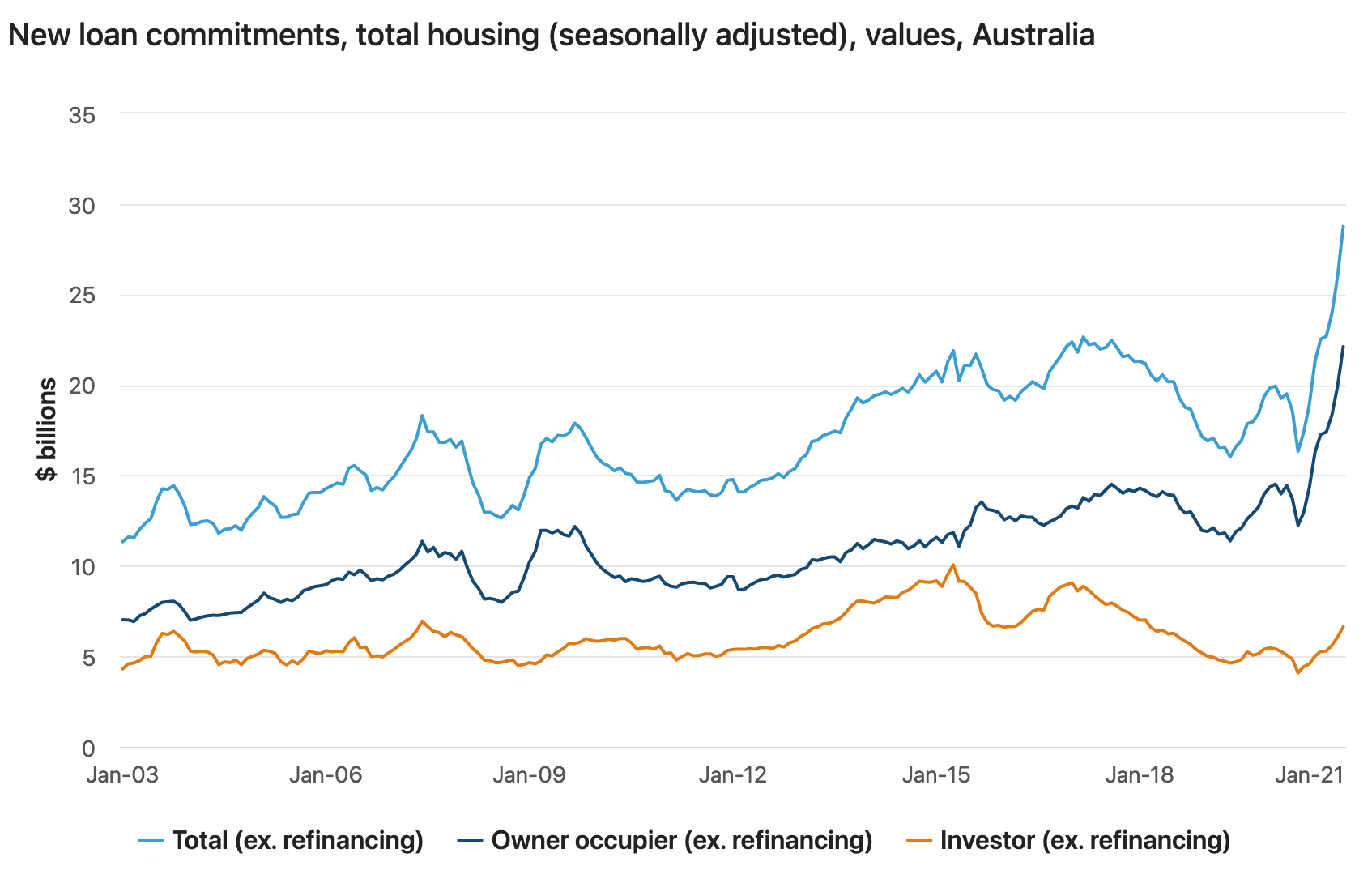

What’s interesting about the situation in Australia is that the housing boom is being driven by owner occupiers, not investors.

According to Australian Bureau of Statistics figures, owner occupiers made up 77% of the value of new home loan lending in January. Investors only made up 23%.

Source: ABS

If investors come back into the market and the market continues booming, Domain senior research analyst Dr Nicola Powell says first home buyers could be squeezed out.

“While it’s still too early to make firm predictions, historically low interest rates and a better economic outlook for Australia will likely see investors come back to the market,” Dr Powell told Savings.com.au.

“House prices are for the most part, rising faster than incomes so will no doubt have an impact on how accessible certain parts of the market are for first home buyers.”

While reports of the RBA being unlikely to raise the cash rate for at least another three years may be good news for some, Dr Powell said there comes a point when the implications of low interest rates begin to outweigh the benefits.

“Ultimately, this is likely to lead to fewer suburbs where buying is cheaper than renting because record-low interest rates generate higher demand for homes, giving people greater purchasing power.

“Falling and low interest rates ignite market activity, and values increase as a response.

“Housing affordability is challenged in the face of rising prices to a point that the benefits of lower mortgage rates become diminished.”

Image by Savings.com.au

Ready, Set, Buy!

Learn everything you need to know about buying property – from choosing the right property and home loan, to the purchasing process, tips to save money and more!

With bonus Q&A sheet and Crossword!

Rachel Horan

Rachel Horan

Emma Duffy

Emma Duffy