To help you decide which one you should use, here we’ll compare self-managed super funds with retail and industry super funds based on fees, returns and how much effort they require to run.

Need somewhere to store cash and earn interest? The table below features introductory and ongoing savings accounts with some of the highest interest rates on the market.

| Bank | Savings Account | Base Interest Rate | Max Interest Rate | Total Interest Earned | Introductory Term | Minimum Amount | Maximum Amount | Linked Account Required | Minimum Monthly Deposit | Minimum Opening Deposit | Account Keeping Fee | ATM Access | Joint Application | Tags | Features | Link | Compare |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

4.40% p.a. | 5.75% p.a. Intro rate for 4 months then 4.40% p.a. | $980 | 4 months | $0 | $250,000 | $0 | $0 | $0 | Featured |

| |||||||

4.75% p.a. | 5.35% p.a. Intro rate for 4 months then 4.75% p.a. | $1,001 | 4 months | $0 | $249,999 | $0 | $0 | $0 | Featured |

| |||||||

2.85% p.a. | 3.55% p.a. Intro rate for 4 months then 2.85% p.a. | $621 | 4 months | $0 | $49,999 | $0 | $0 | $0 | Featured |

| |||||||

– Bonus rate of 5.50% Rate varies on savings amount. | 5.50% p.a. | $1,128 | – | $0 | $100,000 | $0 | $0 | $0 | Featured *Rate varies on savings amount |

| |||||||

0.55% p.a. Bonus rate of 4.95% Rate varies on savings amount. | 5.50% p.a. | $1,128 | – | $0 | $100,000 | $1,000 | $0 | $0 |

|

What is an SMSF?

A self-managed super fund (SMSF) is basically a superannuation fund you run yourself with up to four different members (trustees). This is different to a regular super account offered by a superannuation provider which manages your retirement funds for you. Those that choose an SMSF over a regular super fund typically value the additional level of control they have over their retirement funds, such as where and how much of it is invested.

When it comes to super funds, there are actually multiple different types.

What is a retail super fund?

Retail funds are super funds offered by banks and investment companies. For example, super funds offered by the big banks (ANZ, NAB, Commbank etc.) are retail super funds. Other banks like ING, AMP and Suncorp are also examples of retail banks. These funds tend to have a wide range of investment options, can have higher fees than other types of accounts, and importantly, the company that owns the fund has an incentive to generate a profit for its shareholders. This isn’t always the case however, and we’ll go into returns and fees further down this page.

What is an industry super fund?

Industry funds used to be only for those working in certain industries, but are now mostly open to the public. These are not-for-profit funds, and all profits are reinvested back into the funds. Industry super funds claim this allows them to charge lower fees and generate greater investment returns. Well-known industry funds you might have heard of include the likes of AustralianSuper, HOSTPLUS, Sunsuper and Cbus.

Other types of super funds aside from SMSFs include:

-

MySuper funds: My Super is an Australian Government scheme offering employees low-fee super funds as a default option, and is intended to replace the existing default accounts most super funds offer. From 1 July 2017, all member accounts in default investment options will be required to be invested in MySuper products, which generally have low fees, limited investment options (balanced) and basic levels of insurance cover.

-

Corporate funds: Corporate funds, according to ASIC, are arranged by the employer for their employees. A corporate fund will be the default fund nominated by the employer when hiring someone new - the employee does not have to choose this fund. Corporate super funds tend to be managed by bigger super providers and have a wide range of investment options as well as low-medium fees. Corporate funds run by the employer or an industry fund will usually return all profits to members, and retail funds will return some profits.

-

Public sector funds: Public sector funds are for government employees. They usually have fewer investment options and generally have low fees.

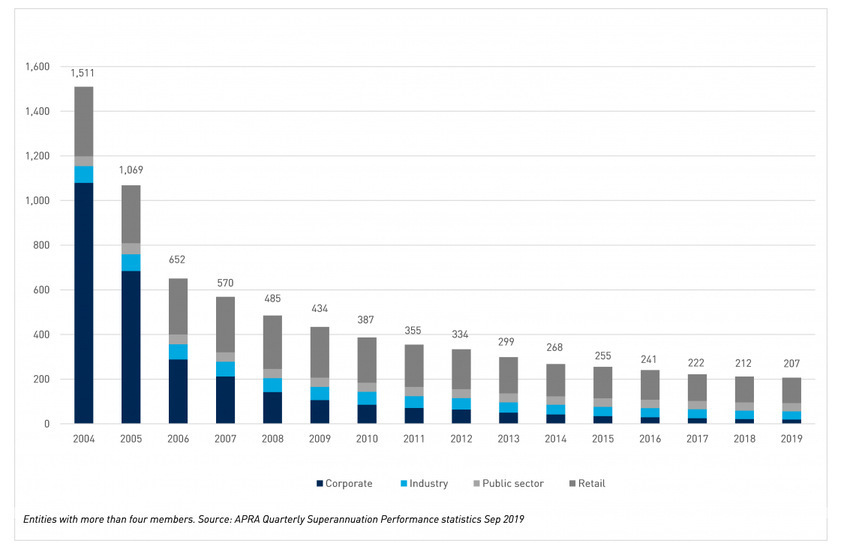

A timeline of the popularity of the different types of super funds - the industry appears to have been consolidated to less than one-seventh (or 14%) of the original number.

How are SMSFs and super funds different?

There are some key differences between regular super funds and SMSFs, aside from just being differently managed. According to the ATO, they’re different in the following areas:

|

SMSF |

Other super funds |

|

|---|---|---|

|

Members and trustees |

Can have a maximum of four members. All members are involved in managing the SMSF. |

Usually no limit on the number of members, managed by licensed trustees. |

|

Responsibility |

Trustees are expected to have knowledge of tax and super laws and must make sure their fund complies with those laws. Trustees can be fined for breaching the law. |

Compliance risk is borne by the professional licensed trustee - no risk for you. |

|

Investment |

Trustees develop and implement the fund's investment strategy, and make all investment decisions |

You generally can't choose the specific assets your super will be invested in, but you can have some control over the mix of investments and the risk level. |

|

Insurance |

Trustees must consider whether to purchase insurance, insurance premiums may be higher than in other super funds. |

Most offer insurance cover to members, is also an option. Can cost less as large funds can get discounted premiums. |

|

Regulation |

Regulated by the ATO, trustees are required to engage with the ATO to manage their fund. |

Regulated by the Australian Prudential Regulation Authority (APRA), members don't have to engage with APRA in most cases. |

|

Complaints/disputes |

Disagreements can be resolved through alternative dispute resolution techniques or in court, at the members' own expense. |

Members have access to the Australian Financial Complaints Authority (AFCA) and may be eligible for statutory compensation. |

Source: The Australian Taxation Office (ATO)

So to summarise, SMSFs come with a much higher degree of personal responsibility, and you can be fined if you don’t meet the regulations imposed by the ATO. This of course comes with a higher degree of freedom, while super funds outsource all of this nitty-gritty to a fund manager.

In addition to these areas, SMSFs and super funds can be quite different when it comes to both fees and returns, although the level to which they’re different will depend on the fund and who is running it.

What gives better returns? SMSFs, retail funds or industry funds?

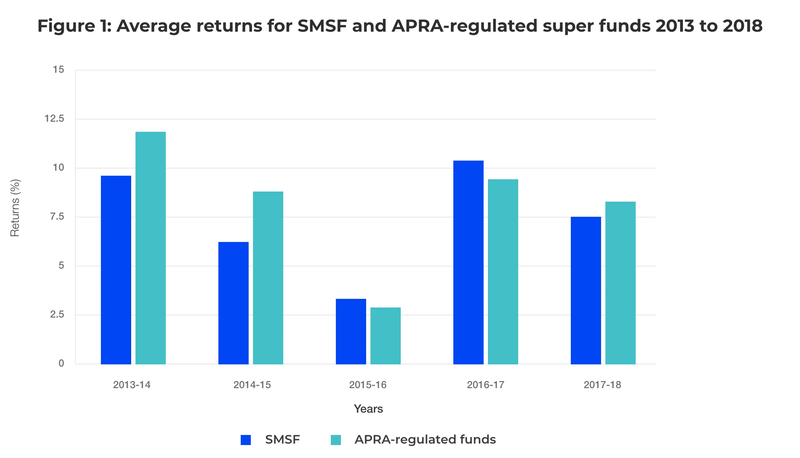

Again, this question will ultimately come down to each fund itself, and past returns are no guarantee of future returns. An SMSF that performed badly one year could still outperform another super fund that performed well in another year. That being said, SMSFs have historically struggled to beat APRA regulated super funds, with regular super funds outperforming them on average in most of the last few financial years.

Source: Self-managed super funds: a statistical overview 2017–18, Australian Taxation Office

In this graph, we see that from 2013 to 2018, SMSFs only outperformed regular super funds in 2016-17, when they, on average, achieved growth of 10.2% compared to 9.1% for super funds. But in most other years, regular super funds have done better, and this could be put down to a number of factors, be it a lack of investment know-how, lower risk appetites, or fees that are too high in relation to the amount invested (more on this below).

|

Fund type |

2017–18 |

2016–17 |

2015–16 |

2014–15 |

2013–14 |

|---|---|---|---|---|---|

|

SMSFs |

7.5% |

10.2% |

3.1% |

6.0% |

9.7% |

|

APRA-regulated funds |

8.5% |

9.1% |

2.9% |

8.9% |

11.7% |

Average returns for SMSFs and APRA-regulated funds, 2013–14 to 2017–18. Source: ATO.

Between retail and industry super funds, this again depends on the fund, but generally speaking industry funds have the edge. In 2018 the Productivity Commission noted in a draft report that when comparing MySuper products (basic super funds) over 10 years, 14 out of 16 retail funds underperformed their benchmarks, compared to 7 of the 33 industry funds surveyed.

In contrast, 23 industry funds performed ‘above benchmark’, compared to one retail fund.

But remember, past returns are no guarantee of future returns.

SMSF vs super funds: Fees

Overall, SMSFs can be quite expensive to run. According to the Australian Taxation Office’s (ATO) statistical overview of SMSFs in 2017/18:

- The average total cost of running an SMSF was $14,879; and

- The median total cost of running an SMSF was $7,710

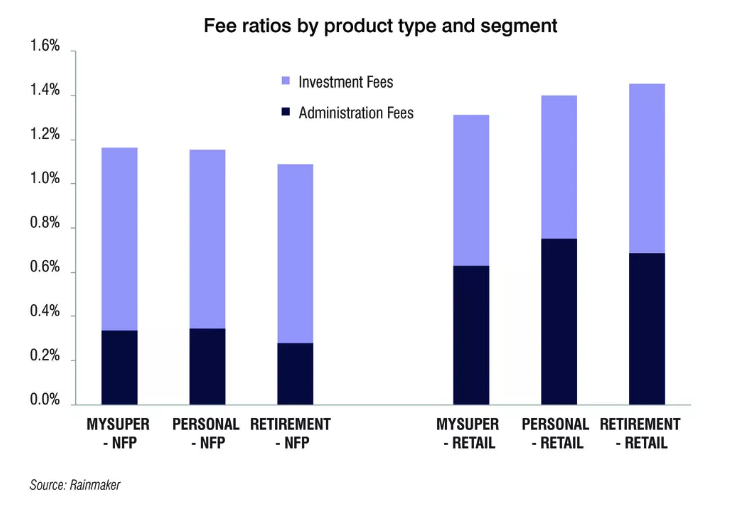

These costs can include establishment/upfront costs, ongoing/operating costs and investment management costs. Regular super funds tend to be much cheaper. A 2019 Rainmaker report on super fees found the average super fund charges $2,400 per year on average - the cost of the average household energy bill. That’s roughly 1/6th of the cost of the average SMSF. Retail funds again seem to charge higher fees on average compared to industry funds.

What should you use: SMSF or a super fund?

In our article ‘A guide to SMSF fees’, we discuss the issue of when an SMSF is “worth it” or not. A general rule of thumb in investing is that you shouldn’t be paying more than 1% of your overall investment balance in fees. If you are, then the investment may be generally deemed poorer value for money, although you may still prefer the higher cost in exchange for greater control.

|

Fund size |

Operating expenses |

Total expenses |

|---|---|---|

|

$1–$50k |

8.2% |

15.4% |

|

>$50k–$100k |

3.4% |

7.3% |

|

>$100k–$200k |

2.2% |

6.7% |

|

>$200k–$500k |

1.3% |

3.7% |

|

>$500k–$1m |

0.8% |

1.7% |

|

>$1m–$2m |

0.5% |

1.0% |

|

>$2m |

0.3% |

0.7% |

Source: ATO

Based on these ATO figures, only SMSF investments with over $1 million in them would pass this benchmark, while in 2019, ASIC cited a Productivity Commission (PC) report stating that SMSFs with balances below $500,000 produce lower returns on average, after expenses and tax, when compared to industry and retail super funds.

“SMSFs may be an attractive option for investors wanting more control over their superannuation investment strategy, but it requires real skill, care and diligence to manage your own superannuation,” ASIC Commissioner Danielle Press said at the time.

“SMSFs are not for everyone simply because not everyone can meet the significant time, costs, risks and obligations associated with establishing and running one.”

Meanwhile, ASIC’s report stated: “SMSFs are not an appropriate investment option for people who want a simple superannuation solution, particularly if they have a low level of financial literacy or limited time to manage their own financial affairs”.

[Read: Is a self-managed super fund right for you?]

Savings.com.au’s two cents

SMSFs and regular super funds are similar, yet different, and are generally suited to different types of people. In short, SMSFs are generally better suited to those who:

- Have a higher balance;

- Have a greater than average financial literacy;

- Have more time on their hands; and

- Understand the legal obligations and risks associated with running one.

On the other hand, an SMSF might not be the best choice for you if:

- You have a low-medium superannuation balance;

- You’re not highly financially literate;

- You aren’t willing to put in the time or money to run an SMSF; and

- You’re not prepared to take on the legal risks of running an SMSF

If you want a hands-off way to invest your retirement savings that is often cheaper and still has the potential to provide high returns, you’re likely better off with a regular super fund. When comparing super funds, you need to compare both the past returns and fees of the funds, as well as the different investment options they provide and the insurance coverage.