If you are looking to live in your property, you need to make sure you are evaluating owner-occupied home loans.

Owner-occupied home loans are available for borrowers who are going to live in the property they purchase. Anyone looking to live in an existing property, build a new one, or renovate, fit the criteria.

This differs from an investment loan, which is for someone purchasing a property in order to rent it out to make money off rental yield or capital gain.

Advertisement

Buying a home or looking to refinance? The table below features home loans with some of the lowest interest rates on the market for owner occupiers.

| Lender | Home Loan | Interest Rate | Comparison Rate* | Monthly Repayment | Repayment type | Rate Type | Offset | Redraw | Ongoing Fees | Upfront Fees | LVR | Lump Sum Repayment | Additional Repayments | Split Loan Option | Tags | Features | Link | Compare |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

6.04% p.a. | 6.06% p.a. | $2,408 | Principal & Interest | Variable | $0 | $530 | 90% | Featured 4.6 Star Customer Ratings |

| |||||||||

5.99% p.a. | 5.90% p.a. | $2,396 | Principal & Interest | Variable | $0 | $0 | 80% | Featured Apply In Minutes |

| |||||||||

6.09% p.a. | 6.11% p.a. | $2,421 | Principal & Interest | Variable | $0 | $250 | 60% | Featured Unlimited Redraws |

|

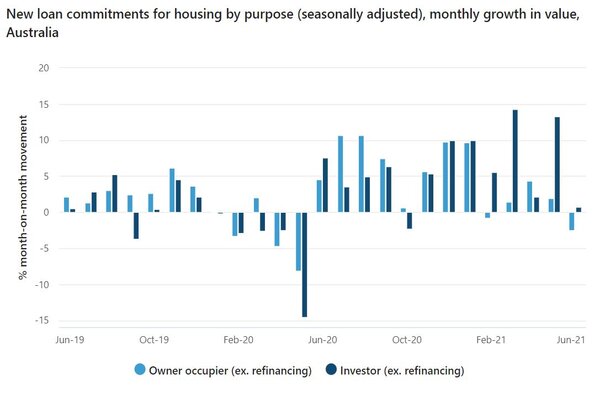

Australian Bureau of Statistics data shows the total value of new loan commitments in Australia, with the majority being owner-occupier loans.

Why does it matter?

When you're applying for a home loan to buy a house, you need to specify that you're applying for an owner-occupier loan, not an investor loan.

This will impact the interest rate you repay the loan to your lender because lenders generally consider an owner-occupied loan to be safer than an investment loan, and thus, have cheaper rates.

This is largely due to the riskier nature of rental markets, and additional costs associated with being an investment property owner like property management fees, and insurance.

Reserve Bank data from July 2021 shows the average discounted variable rate for an owner occupier was 3.60% p.a. compared to the investor average 4.08% p.a.

It’s important to compare home loans & interest rates.

Recently, investment home loans have been on the rise, as per the ABS table below.

What are lenders looking for?

When applying for an owner-occupied home loan, lenders will consider your borrowing power. Borrowing power is how much a lender is willing to give you to purchase a home. This amount is dictated by your income, savings, assets, and debts you have.

Often lenders will accept a smaller deposit for an owner-occupied loan than an investment loan as it is considered less risky. A common deposit is 20% of the property cost, meaning 80% of the cost is lent to you, which you will pay back over a set amount of time (usually 20-30 years) with interest.

-

This ratio of how much you pay and how much your lender loans you, is called Loan to Value Ratio (LVR).

-

Any less than a 20% deposit usually means you will have to pay Lenders Mortgage Insurance (LMI), though some lenders waive LMI if you have a 15% deposit.

You will be required to pay back your loan with interest, which can be fixed, variable, or both.

Principal & Interest vs Interest Only Payments

A common feature of any given home loan is whether you have to pay principal & interest (P&I), or interest only (IO).

Interest-only loans have typically been more popular in the investment home loan space as they allow the investor to manage cashflow while sorting out tenants and realising capital gain.

However, the more popular option for owner occupiers has traditionally been P&I loans. And for good reason: RBA data shows the average standard variable rate (SVR) for owner occupiers paying interest only on a home loan is 5.06% p.a. By comparison, the average SVR on a P&I loan is 4.52% p.a.

Fixed vs Variable interest rates

If you are looking to buy a home, it's important to compare fixed and variable rates.

A fixed interest rate home loan is a home loan with the option to lock in (or ‘fix’) your interest rate for a set period of time (usually between one and five years).

A variable rate home loan is a home loan where your interest rate will move (or ‘vary’) with changes to the market. This means your interest rate can rise or fall over the term of your loan.

Both have their pros and cons, and it's important to do your own research and seek financial advice to see what is best for you and your situation.

However, in recent years, fixed rates have become more competitive. RBA data shows the average owner occupier rate for a three-year fixed home loan is 2.19% p.a. Just three years prior it was more than double that number.

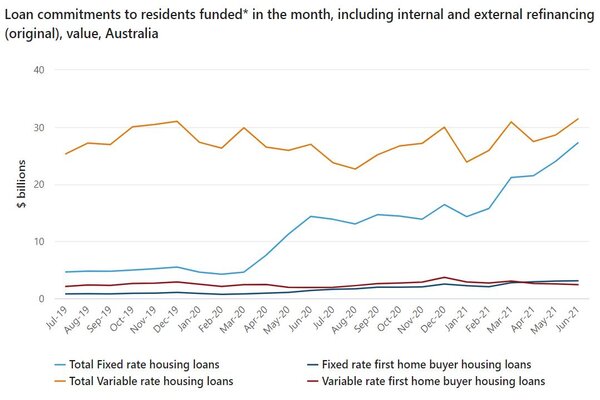

ABS data also shows the total value in variable rate home loans is higher than fixed, however this gap reduced over the past three years.

What if I want to move out of my owner-occupied home and rent it out?

If circumstances change and you choose to move out of your home in order to rent it out to a third party, you need to discuss with your lender first.

Changing your owner-occupied home into an investment means changing the loan to an investment loan which will mean a different interest rate.

Failing to discuss any changes on your owner-occupied home can result in being charged with occupancy or mortgage fraud.

There is plenty to consider when applying for a owner-occupied home loan. Remember to compare interest rates, seek qualified financial advice and always update your lender with any changes to your circumstances to avoid being hit with hidden fees or fines.

Image by Josue Michel via Unsplash

Ready, Set, Buy!

Learn everything you need to know about buying property – from choosing the right property and home loan, to the purchasing process, tips to save money and more!

With bonus Q&A sheet and Crossword!

Emma Duffy

Emma Duffy

Harrison Astbury

Harrison Astbury

Rachel Horan

Rachel Horan

Brooke Cooper

Brooke Cooper